- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:86,200 KRW 41,500 KRW

🎯 Target Price:125,000 KRW 62,000 KRW

📈 Upside Potential: 45.0%

*Updated Market Report: June 2026*

Doosan Enerbility Valuation: Nuclear Renaissance and SMR Manufacturing Leadership

Doosan Enerbility (KRX: 034020), formerly known as Doosan Heavy Industries & Construction, is South Korea’s leading heavy industrial company and a primary supplier of power generation equipment globally. The company has successfully completed a massive structural pivot away from coal-fired power plants, positioning itself as a core player in the global clean energy transition. Its main growth drivers are large-scale nuclear reactors, Small Modular Reactors (SMRs), gas turbines, and wind power installations.

With the global energy sector experiencing a structural “nuclear renaissance” driven by AI data center power demands and carbon-neutral mandates, Doosan Enerbility is seeing a rapid expansion of its order backlog. This report delivers an in-depth valuation of Doosan Enerbility, analyzing its production capacity, key strategic partnerships in the United States, global reactor bidding pipelines, and long-term financial trajectory.

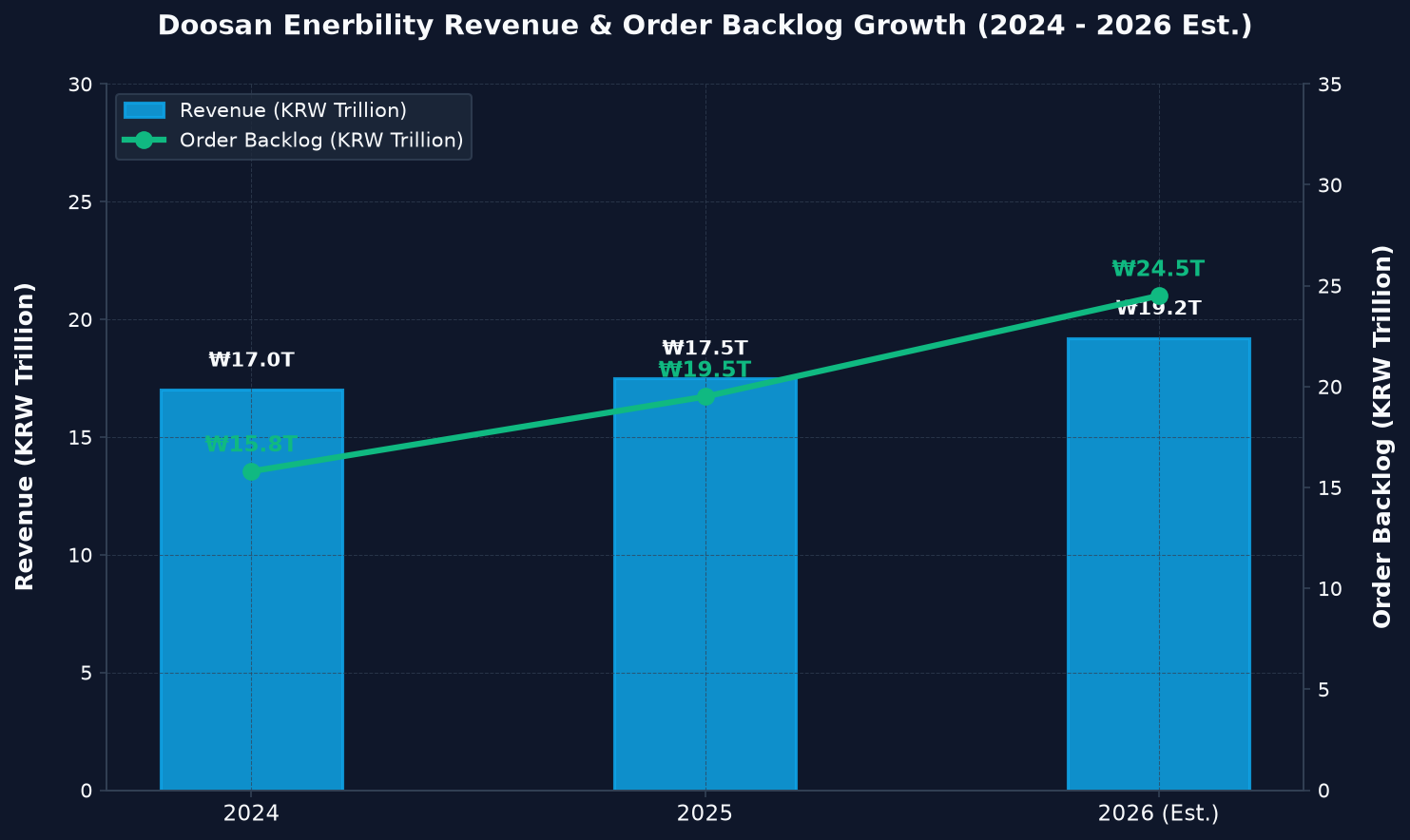

📈 Financial Trajectory and Order Backlog Dynamics

Doosan Enerbility’s recovery is structurally supported by a growing backlog of high-margin power equipment contracts. The capital-intensive nature of utility-scale power projects means that today’s backlog additions determine the company’s revenue and cash flow profiles over the next three to five years.

Three-Year Key Financial and Backlog Trajectory

The following table highlights the steady revenue recovery and the sharp rise in order backlog projected through the end of fiscal year 2026, showcasing the acceleration of nuclear and gas turbine contract signings.

| Financial Metric | 2024 | 2025 | 2026 (Est.) | Operating Margin Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩17.0T | ₩17.5T | ₩19.2T | 8.2% |

| Operating Profit (KRW Trillion) | ₩1.40T | ₩1.60T | ₩2.20T | 9.1% |

| Net Income (KRW Trillion) | ₩0.80T | ₩0.90T | ₩1.50T | 11.5% (Est.) |

Backlog Conversion and Capital Efficiency

As utility infrastructure orders scale, Doosan’s capacity utilization rates at its Changwon foundry and heavy forging plant are approaching optimal capacity. Fixed-cost overhead is diluted across larger order volumes, allowing operating profit margins to expand from historical single digits toward 11.5% in 2026.

Figure: Revenue Scaling and Robust Order Backlog Trajectory

💡 Lingo Check: SMR and Forging Capacity

Let’s clarify two critical technical concepts for the nuclear manufacturing space:

– Small Modular Reactor (SMR – 소형 모듈 원전): Advanced nuclear reactors that have a power capacity of up to 300 MW per unit, which is about one-third of the generating capacity of traditional nuclear power reactors. They are modular, allowing components to be assembled in factories and transported to sites for installation.

– Heavy Forging Plant (주단조 공장): A facility that uses massive hydraulic presses (such as Doosan’s 17,000-ton press) to compress raw steel ingots into dense, seamless components capable of withstanding the high pressure and temperature inside a nuclear reactor pressure vessel.

🚀 SMR Foundry Monopoly: Partnering with US Pioneers

The primary long-term catalyst for Doosan Enerbility is its emerging role as the global “foundry” for SMR designs. SMR developers in the United States and Europe operate under asset-light business models, designing reactors while outsourcing fabrication to specialized heavy industrial manufacturers.

The NuScale Power Alliance

Doosan Enerbility is a strategic equity investor and the primary manufacturing partner of NuScale Power, the first company to receive design approval for an SMR from the US Nuclear Regulatory Commission (NRC). Under current procurement schedules, Doosan is fabricating reactor pressure vessels and steam generator modules for NuScale’s landmark projects, providing the company with an early-mover advantage in SMR supply chain commercialization.

Expanding Alliances: X-energy and TerraPower

Doosan has expanded its manufacturing agreements to include other leading SMR designers, such as X-energy (high-temperature gas-cooled reactors) and TerraPower (sodium-cooled fast reactors backed by Bill Gates). By serving as the common manufacturer for competing SMR technologies, Doosan Enerbility functions as a diversified infrastructure play on the SMR sector.

🔬 Global Nuclear Export Pipelines & Turbine Localization

While SMRs represent the future growth curve, large-scale nuclear power plant exports and domestic gas turbine localization drive near-term cash flows.

Global Nuclear Export Strategy

South Korea’s nuclear consortium—led by Korea Electric Power Corporation (KEPO – 한국전력) and Korea Hydro & Nuclear Power (KHNP – 한국수력원자력)—is actively bidding for major nuclear contracts in Europe and the Middle East. As the sole domestic manufacturer of nuclear steam supply systems (NSSS), including reactor pressure vessels, steam generators, and steam turbines, Doosan Enerbility secures a substantial portion of any export contract won by the consortium.

Gas Turbine Localization and Hydrogen Co-firing

Doosan Enerbility is one of only five companies in the world capable of manufacturing large-scale gas turbines for power plants. The company has successfully localized its 270MW and 380MW gas turbine models, replacing imported turbines in South Korea’s domestic power grid. Doosan is currently developing hydrogen gas turbines capable of co-firing hydrogen and natural gas, aligning its turbine business with long-term zero-carbon targets.

⚖️ Valuation & Peer Multiples Analysis

To assess the investment potential of Doosan Enerbility, we evaluate its valuation metrics against global industrial engineering peers.

Multiples Matrix (June 2026)

– Doosan Enerbility (KRX: 034020): Forward P/E 18.5x | EV/EBITDA 9.2x | Net Debt/EBITDA 1.8x

– General Electric (NYSE: GE): Forward P/E 24.5x | EV/EBITDA 14.8x | Net Debt/EBITDA 1.1x

– Westinghouse Electric (Private): Estimated P/E equivalent 22.0x

– IHI Corporation (TYO: 7013): Forward P/E 16.2x | EV/EBITDA 8.1x | Net Debt/EBITDA 2.2x

Valuation Perspective

Doosan Enerbility trades at a forward P/E of 18.5x, reflecting a discount compared to global clean energy leaders like GE. However, it commands a premium relative to traditional domestic heavy industrials due to its dominant positioning in SMR manufacturing. As international nuclear build programs accelerate and SMR manufacturing runs begin commercial scaling, the company’s capital efficiency and margins are positioned to rise, driving a valuation re-rating.

⚠️ Potential Risk Factors

Investors should note the following risks before committing capital:

– Project Execution and Delays: Large-scale nuclear projects are subject to strict regulatory oversight, and construction delays can defer revenue recognition and increase financing costs.

– Geopolitical and IP Disputes: Intellectual property disputes between KHNP and foreign reactor designers (such as Westinghouse) regarding export technologies can delay contract finalization.

– Raw Material Volatility: Sharp increases in the prices of nickel, chromium, and specialized steel alloys can compress Doosan’s manufacturing margins on fixed-price contracts.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 86,200 KRW

🎯 Target Price: 125,000 KRW

Doosan Enerbility is a premier investment vehicle to capture the global nuclear energy renaissance and SMR scaling. As the exclusive manufacturer of nuclear components in South Korea and a strategic partner to leading US SMR developers, the company has built a highly defensive competitive moat. Supported by a rising ₩24.5T backlog and successful gas turbine localization, the company is entering a multi-year growth cycle. We recommend accumulating shares before SMR commercial deliveries begin driving margin expansion.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*