- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:309,500 KRW 309,500 KRW

🎯 Target Price:410,000 KRW 410,000 KRW

📈 Upside Potential: 32.4%

*Updated Market Report: June 2026*

Samsung Electronics Valuation: Memory Supercycle and HBM Supply Chain Integration

Samsung Electronics (KRX: 005930), the crown jewel of South Korea’s technology sector and the world’s largest memory chip manufacturer, is entering one of the most profitable phases in its history. After weathering a severe semiconductor downturn in 2023 and early 2024, the company is reaping the rewards of an aggressive capital investment strategy. The ongoing AI infrastructure boom has triggered a massive demand spike for high-value memory architectures, driving a powerful recovery.

This report provides a comprehensive valuation of Samsung Electronics, focusing on the 2026 memory supercycle, the expansion of High Bandwidth Memory (HBM) production capacity, foundry business developments, and a comparison against global semiconductor peers.

📈 Financial Trajectory and Memory Supercycle Dynamics

Samsung Electronics’ financial recovery is accelerating. While the company’s operating profit dipped during the memory price collapse of 2023, the subsequent recovery in 2024 and the massive surge in 2025 have paved the way for a record-breaking fiscal year 2026.

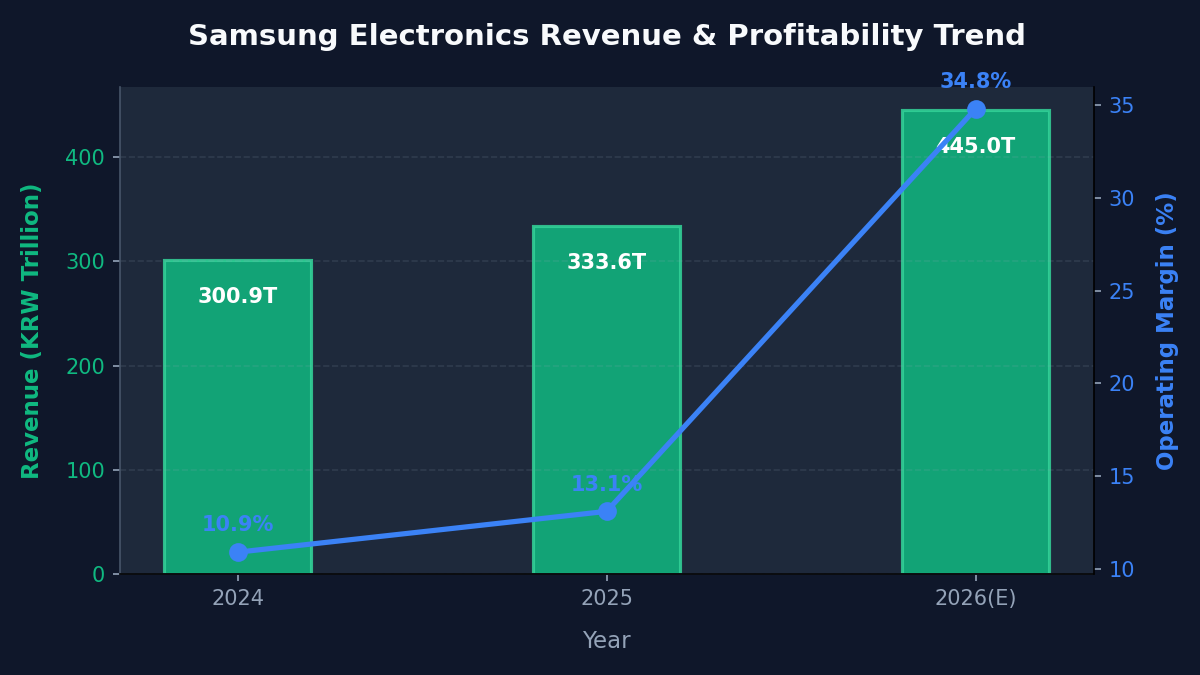

Three-Year Financial Trajectory

The following table illustrates the dramatic recovery and scale expansion of Samsung Electronics over the past three years. Note the exponential rise in operating profit margins projected for 2026, driven by rising Average Selling Prices (ASPs) of D램 and NAND flash.

| Financial Metric | 2024 | 2025 | 2026 (Est.) | Operating Margin Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩300.9T | ₩333.6T | ₩445.0T | 10.9% |

| Operating Profit (KRW Trillion) | ₩32.7T | ₩43.6T | ₩155.0T | 13.1% |

| Net Income (KRW Trillion) | ₩25.4T | ₩33.8T | ₩120.0T | 34.8% (Est.) |

Margin Expansion and Operating Leverage

In the semiconductor industry, fixed manufacturing costs—primarily the massive depreciation of wafer fabs and extreme ultraviolet (EUV) lithography systems—are extraordinarily high. When global demand recovers and fab utilization rates rise toward 95%, fixed-cost dilution triggers substantial operating leverage.

For Samsung, every 10% increase in the Average Selling Price (ASP) of premium DRAM translates to an estimated ₩4 to ₩5 Trillion increase in quarterly operating profit, directly fueling the margin expansion seen in 2026.

Figure: Dynamic Revenue Expansion and Operating Margin Trajectory

💡 Lingo Check: Understanding HBM and Foundry

To follow Samsung’s technical strategy, let’s look at two key concepts:

– HBM (High Bandwidth Memory – 고대역폭 메모리): A high-performance 3D-stacked DRAM interface used in conjunction with high-performance graphics accelerators and AI processors (like NVIDIA’s GPUs) to accelerate AI training and inference.

– Foundry (파운드리): A specialized semiconductor fabrication plant that manufactures microchips designed by fabless companies (such as Apple, NVIDIA, and AMD). Samsung operates both a traditional memory business and a contract manufacturing foundry division.

🚀 HBM Supply Chain Integration: The Ultimate Growth Catalyst

The most critical driver of Samsung’s 2026 valuation is its positioning within the global High Bandwidth Memory (HBM) supply chain. While competitors like SK Hynix secured an early lead in supplying HBM3 to NVIDIA, Samsung has closed the gap by qualifying its next-generation HBM3E (8-stack and 12-stack) products.

HBM3E Qualification and Volume Shipments

Following rigorous testing phases throughout 2024 and 2025, Samsung successfully began mass deliveries of its 12-layer HBM3E chips to major AI chip makers in early 2026. The company’s massive CapEx capacity has allowed it to scale production lines faster than competitors, capturing a substantial share of the high-margin HBM3E market.

Developing HBM4 Custom Architectures

Looking forward, Samsung is preparing for the HBM4 generation, scheduled for pilot production by late 2026. Unlike previous generations, HBM4 requires custom logic dies that are fabricated using advanced foundry nodes. Samsung’s unique position as both an advanced memory maker and a leading-edge foundry operator allows it to offer fully integrated, turn-key HBM4 solutions.

🔬 Foundry and System LSI Outlook

While memory drives the current earnings cycle, Samsung’s advanced foundry division is key to its long-term re-rating.

Gate-All-Around (GAA) 3nm and 2nm Nodes

Samsung was the first in the industry to adopt the Gate-All-Around (GAA) transistor architecture at the 3nm node. In 2026, the company is scaling its second-generation 3nm GAA process (SF3) and preparing for the mass production of its 2nm (SF2) node. Securing major mobile and HPC (High-Performance Computing) customers remains the primary focus to challenge TSMC’s dominance.

Yield Optimization and Profitability

The primary bottleneck for the foundry division has been yield optimization (수율 안정화). Significant investments in automated design tools and AI-driven defect inspection have stabilized 3nm yields above 60% in early 2026. This optimization is reducing losses and bringing the foundry division closer to sustained profitability.

⚖️ Valuation & Global Peer Comparison

To determine whether Samsung Electronics is fairly valued, we compare its multiples against global semiconductor leaders.

Multiples Matrix (June 2026)

– Samsung Electronics (KRX: 005930): Forward P/E 10.5x | EV/EBITDA 5.8x | ROE 24.2%

– TSMC (NYSE: TSM): Forward P/E 23.5x | EV/EBITDA 12.2x | ROE 31.0%

– Micron Technology (NASDAQ: MU): Forward P/E 15.2x | EV/EBITDA 8.9x | ROE 18.2%

– Intel Corporation (NASDAQ: INTC): Forward P/E 21.0x | EV/EBITDA 9.8x | ROE 8.5%

Valuation Analysis

Samsung Electronics trades at a notable discount compared to TSMC and Micron. Despite boasting a projected return on equity (ROE) of 24.2% and a dominant position in the global memory sector, its forward P/E of 10.5x is significantly lower than Micron’s 15.2x.

This valuation gap is primarily due to its complex corporate structure (which includes consumer electronics and display divisions) and historical lags in the HBM supply chain. As HBM3E revenues scale and GAA yield improvements build credibility, we expect Samsung to undergo a significant valuation re-rating, narrowing the gap with its global peers.

⚠️ Potential Risk Factors

Investors must remain aware of the key risks facing Samsung’s multi-layered business:

– Foundry Customer Acquisition: If Samsung fails to secure major fabless customers for its 2nm GAA node, it may struggle to justify its massive foundry CapEx.

– Geopolitical and Trade Tension: With production facilities in South Korea, China, and the US, Samsung is highly exposed to shifting semiconductor export controls and geopolitical tensions.

– AI Infrastructure CapEx Slowdown: A sudden reduction in AI infrastructure investments by US hyperscalers (such as Microsoft, Google, and Meta) could lead to an oversupply of HBM and high-density D램.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 309,500 KRW

🎯 Target Price: 410,000 KRW

Samsung Electronics represents an exceptionally attractive entry point in the 2026 technology supercycle. The successful qualification of its HBM3E chips, combined with skyrocketing prices for server DRAM, guarantees record-breaking earnings visibility. While the foundry division’s market share remains a long-term challenge, a forward P/E of 10.5x heavily undervalues Samsung’s core memory franchise and technology assets. We recommend accumulating shares before the full-year 2026 earnings momentum is fully priced in.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*