- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:577,000 KRW 242,000 KRW

🎯 Target Price:820,000 KRW 330,000 KRW

📈 Upside Potential: 42.1%

*Updated Market Report: June 2026*

HD Hyundai Heavy Industries Valuation: Clean Shipping Cycle and Naval MRO Expansion

HD Hyundai Heavy Industries (KRX: 329180), the flagship shipbuilding subsidiary of HD Hyundai Group (formerly Hyundai Heavy Industries Group), is the world’s largest shipbuilder by production capacity. Operating its primary yard in Ulsan, South Korea, the company manufactures commercial vessels, offshore engineering platforms, and naval combatants.

As global maritime environmental regulations force shipowners to replace legacy fleets, the commercial shipping sector is entering a multi-year clean vessel cycle. This report provides an in-depth valuation of HD Hyundai Heavy Industries, focusing on the Clarkson Newbuilding Price Index trend, eco-friendly propulsion technologies (LNG, methanol, and ammonia), expansion into United States naval MRO (maintenance, repair, and overhaul) services, and financial trajectory through 2026.

📈 Financial Trajectory & Shipbuilding Price Cycles

In the shipbuilding sector, profitability is a lagging indicator of contracting cycles. Because commercial vessel manufacturing takes two to three years from contract signing to final delivery, the low-price orders signed during market downturns can weigh on margins even after shipping rates recover. Conversely, the high-price, eco-friendly contracts signed in recent years are driving a strong margin expansion through 2026.

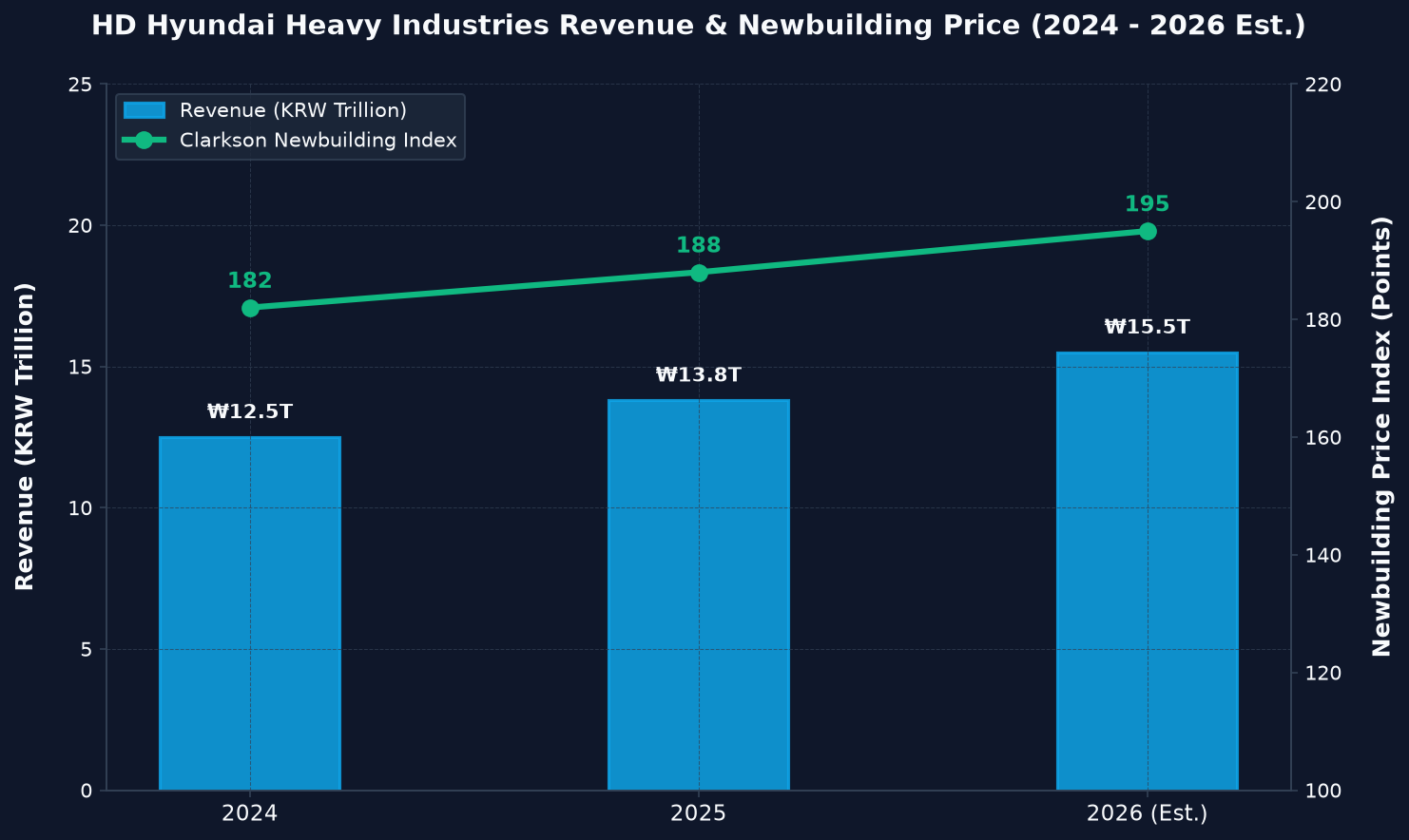

Three-Year Key Financial and Pricing Trajectory

The following table shows the financial recovery of HD Hyundai Heavy Industries over the past three years. Note the rise in operating profit margins as higher-priced contracts are recognized upon delivery.

| Financial & Market Metric | 2024 | 2025 | 2026 (Est.) | Operating Margin Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩12.5T | ₩13.8T | ₩15.5T | 4.3% |

| Operating Profit (KRW Trillion) | ₩0.54T | ₩0.72T | ₩1.20T | 5.2% |

| Net Income (KRW Trillion) | ₩0.32T | ₩0.45T | ₩0.85T | 7.7% (Est.) |

Rising Asset Turnovers and Dilution of Steel Plate Costs

The key cost driver in shipbuilding is thick steel plates (후판), which represent up to 20% of commercial vessel manufacturing costs. As global iron ore and coking coal prices stabilize, steel plate prices are moderating. Combined with high shipyard utilization rates and rising delivery prices, this cost stabilization is expanding operating margins toward 8% by late 2026.

Figure: Revenue Expansion and Rising Clarkson Newbuilding Index (2024 – 2026)

💡 Lingo Check: Newbuilding Index and Dual-Fuel Engines

Let’s define two key concepts for the shipbuilding sector:

– Clarkson Newbuilding Price Index (신조선가 지수): An industry-standard index published by Clarkson Research that tracks price changes for newly built commercial vessels. A rising index indicates increasing pricing power for shipyards.

– Dual-Fuel Propulsion (이중연료 추진): Marine engines capable of running on both traditional fuel oil and alternative clean fuels (such as liquefied natural gas, methanol, or ammonia), allowing vessels to comply with strict international emission standards.

🚀 Eco-friendly Fleet Renewal: Capturing the Green Shift

The primary driver of HD Hyundai Heavy Industries’ competitive advantage is its leadership in alternative marine propulsion. The International Maritime Organization (IMO) has implemented strict carbon intensity indicator (CII) targets, requiring shipowners to transition away from traditional heavy fuel oil.

High-margin LNG and Methanol Carriers

HD Hyundai Heavy Industries is a global leader in the fabrication of membrane-type Liquefied Natural Gas (LNG) carriers and large dual-fuel methanol-enabled container ships. By securing premium pricing slots for these highly technical vessels, the company has built an order backlog extending through 2029, insulating its operations from short-term shipping market volatility.

Ammonia and Hydrogen Developments

Looking toward zero-carbon shipping, the company is securing early orders for Very Large Ammonia Carriers (VLACs). Ammonia is highly regarded as a key hydrogen carrier and a clean marine fuel. HD Hyundai has developed proprietary cargo containment and fuel supply systems, positioning the yard to lead the next generation of zero-emission commercial vessels.

🔬 Special Vessels: Navigating US Navy MRO Integration

While commercial vessels drive bulk revenues, the special vessel division (specializing in destroyers, frigates, and submarines) is entering a high-margin export phase.

US Navy MSRA Qualification

A significant strategic milestone is the company’s progress toward qualifying for the United States Navy’s Master Ship Repair Agreement (MSRA). Due to capacity constraints at domestic US naval shipyards, the US Department of Defense is expanding MRO partnerships to allied nations. Securing MSRA certification allows HD Hyundai to capture high-margin maintenance contracts for US auxiliary and combatant vessels operating in the Indo-Pacific.

Naval Exports to Allied Nations

The special vessel division is actively bidding for naval contracts in Southeast Asia, South America, and Europe. Building on successful frigate deliveries to the Philippine Navy, HD Hyundai is presenting its specialized conventional submarine designs to global buyers, diversifying its defense order pipeline.

⚖️ Valuation & Peer Multiples Comparison

To evaluate whether HD Hyundai Heavy Industries is fairly valued, we compare its metrics against international shipbuilding and industrial peers.

Multiples Matrix (June 2026)

– HD Hyundai Heavy Industries (KRX: 329180): Forward P/E 24.5x | EV/EBITDA 13.8x | ROE 12.8%

– Samsung Heavy Industries (KRX: 010140): Forward P/E 22.0x | EV/EBITDA 12.2x | ROE 11.0%

– Hanwha Ocean (KRX: 042660): Forward P/E 28.2x | EV/EBITDA 15.5x | ROE 8.2%

– Mitsubishi Heavy Industries (TYO: 7011): Forward P/E 22.5x | EV/EBITDA 11.8x | ROE 10.5%

Valuation Analysis

HD Hyundai Heavy Industries commands a premium valuation relative to global industrial conglomerates due to its pure-play exposure to the eco-friendly shipbuilding cycle and advanced naval engineering. Its forward P/E of 24.5x is supported by its market share in premium LNG carriers and its growth potential in naval MRO. As high-margin contracts are delivered, cash flow is positioned to rise, helping to reduce net debt.

⚠️ Potential Risk Factors

Investors must monitor the following key risk factors:

– Labor Shortages: The South Korean shipbuilding industry faces structural labor shortages in welding and outfitting, which could limit production speed.

– Steel Plate Pricing Volatility: Any sudden price increases for shipbuilding-grade steel by domestic steelmakers can compress margins on fixed-price contracts.

– Currency Fluctuations: Since commercial vessel contracts are denominated in USD, a strengthening KRW can impact revenue conversion.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 577,000 KRW

🎯 Target Price: 820,000 KRW

HD Hyundai Heavy Industries is a premier asset to capture the structural clean energy shipping transition. Its technological leadership in dual-fuel propulsion, combined with a multi-year backlog and a premium customer base, ensures high earnings visibility. Supported by expansion into US naval MRO and moderating steel plate costs, we recommend accumulating shares as deliveries of high-value eco-friendly vessels accelerate.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*