- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:1,175,000 KRW 545,000 KRW

🎯 Target Price:1,680,000 KRW 780,000 KRW

📈 Upside Potential: 43.0%

*Updated Market Report: June 2026*

Hanwha Aerospace Valuation: K-Defense Global Dominance and Aerospace Pipeline

Hanwha Aerospace (KRX: 012450), the flagship defense and aerospace division of Hanwha Group, has emerged as one of the fastest-growing military hardware suppliers in the world. Often described as the “Lockheed Martin of Asia,” the company manufactures advanced land defense platforms, precision guided weapons, and aviation engines. Its core products—the K9 Thunder self-propelled howitzer, the Chunmoo multiple launch rocket system (MLRS), and the Redback infantry fighting vehicle (IFV)—are securing massive export contracts globally.

As geopolitical tensions drive global defense spending, Hanwha Aerospace is experiencing record profitability, transitioning from a domestic-oriented contractor to a major exporter. This report provides a comprehensive valuation of Hanwha Aerospace, analyzing its international contract backlog, production speed advantage, aerospace engine integration, and financial trajectory through 2026.

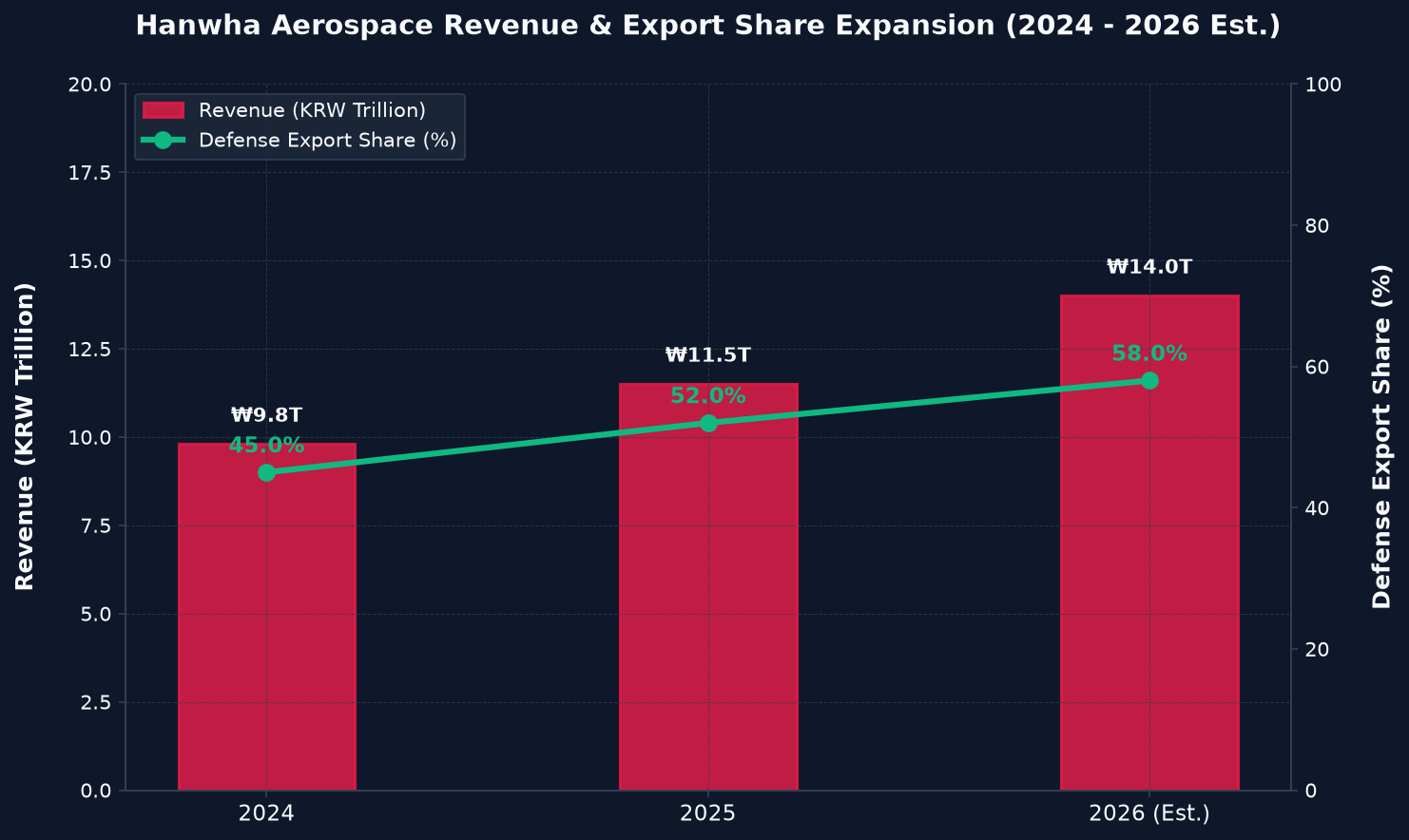

📈 Financial Trajectory & Defense Export Share

The primary catalyst for Hanwha Aerospace’s valuation is the structural shift in its product mix. Export contracts yield significantly higher operating profit margins compared to regulated domestic procurement deals. Consequently, as the share of international sales increases, the company’s profitability is rising.

Three-Year Key Financial and Export Trajectory

The following table shows the financial expansion of Hanwha Aerospace over the past three years. Note the rise in the defense export share and the corresponding expansion of net profit margins projected for 2026.

| Financial & Strategic Metric | 2024 | 2025 | 2026 (Est.) | Operating Margin Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩9.8T | ₩11.5T | ₩14.0T | 9.2% |

| Operating Profit (KRW Trillion) | ₩0.90T | ₩1.20T | ₩1.80T | 10.4% |

| Net Income (KRW Trillion) | ₩0.65T | ₩0.85T | ₩1.30T | 12.9% (Est.) |

Operating Leverage from Export Deliveries

In defense manufacturing, scaling production lines to fulfill multi-billion dollar international batches leads to high asset utilization. With major export milestones—primarily K9 howitzers to Poland and Romania, and Redback IFVs to Australia—ramping up deliveries in 2026, fixed manufacturing costs are diluted. This operating leverage is lifting margins to record heights.

Figure: Revenue Expansion and Accelerating Defense Export Share (2024 – 2026)

💡 Lingo Check: K-Defense and Local Integration

Let’s review two essential terms related to South Korea’s defense strategy:

– K-Defense (K-방산): The collective term for the South Korean defense industry. It is characterized by high production speeds, price competitiveness, and a willingness to transfer technology and establish local manufacturing lines in purchasing countries.

– Multiple Launch Rocket System (MLRS – 다연장로켓): A type of unguided or guided rocket artillery system. Hanwha’s Chunmoo is a high-precision, wheeled MLRS capable of firing various caliber rockets, widely adopted as a key tactical weapon.

🚀 Global Backlog Domination: The Competitive Moat

Hanwha Aerospace’s core competitive advantage lies in its rapid delivery times. Western defense primes often require five to seven years to fulfill major land platform orders due to supply chain constraints and manufacturing backlogs. Hanwha Aerospace, supported by a fully integrated domestic supply chain and automated production lines, can deliver units within one to two years.

The Poland and Romania Portfolios

Following historic framework agreements signed in 2022, Poland has emerged as a major customer for Hanwha. Deliveries of the K9 howitzer and Chunmoo rocket pods have proceeded ahead of schedule. Building on this execution, Romania selected the K9 howitzer in late 2024, adding ₩1.4 Trillion to the order backlog.

Australia and NATO Expansion

Hanwha’s success in winning the Australian Land 400 Phase 3 program with the Redback IFV has validated its technology against top-tier European competitors. By establishing local manufacturing in Geelong, Australia, Hanwha has built a template for technology transfers that it is utilizing to target other NATO nations in Northern and Eastern Europe.

🔬 Aerospace Engines and Space Launcher Pipeline

While defense platforms drive current revenues, the aerospace engine division provides the long-term technology baseline.

Jet Engine Manufacturing and Maintenance

Hanwha Aerospace is the exclusive producer of gas turbine engines for South Korean military aircraft, partnering with global primes like General Electric, Pratt & Whitney, and Rolls-Royce. The company is actively building its capability in maintenance, repair, and overhaul (MRO) services, creating a recurring, high-margin revenue stream as South Korea’s military fleet expands.

The Space Launcher (Nuri) Project

Hanwha Aerospace is the lead systems integration contractor for the Nuri (KSLV-II) space launch vehicle, managed by the Korea Aerospace Research Institute (KARI – 한국항공우주연구원). According to regulatory filings, Hanwha is responsible for manufacturing liquid-fuel rocket engines and assembling the launch vehicle. This positioning establishes the company as the dominant player in South Korea’s commercial space pipeline.

⚖️ Valuation & Global Peer Comparison

To determine whether Hanwha Aerospace is fairly valued, we compare its valuation multiples against global defense primes.

Multiples Matrix (June 2026)

– Hanwha Aerospace (KRX: 012450): Forward P/E 15.5x | EV/EBITDA 9.8x | ROE 25.5%

– Rheinmetall AG (XETR: RHM): Forward P/E 22.0x | EV/EBITDA 13.5x | ROE 22.0%

– General Dynamics (NYSE: GD): Forward P/E 18.2x | EV/EBITDA 12.0x | ROE 19.5%

– L3Harris Technologies (NYSE: LHX): Forward P/E 16.5x | EV/EBITDA 10.5x | ROE 11.2%

Valuation Perspective

Hanwha Aerospace trades at a forward P/E of 15.5x, representing a discount to European peers like Rheinmetall despite boasting a superior ROE of 25.5%. This valuation gap is narrowing as international investors recognize the stability of Hanwha’s order backlog and its unique capability to deliver heavy armor platforms on schedule. The spin-off of non-defense divisions completed in late 2024 has created a pure-play defense investment vehicle, supporting a valuation re-rating.

⚠️ Potential Risk Factors

Investors must monitor the following key risk factors:

– Foreign Exchange Exposure: Since a large portion of revenues is contract-billed in USD or EUR, fluctuations in the KRW exchange rate can impact margins during conversion.

– Localized Production Demands: Rising demands from purchasing countries for local manufacturing and co-development can reduce the profit share captured by Hanwha’s domestic factories.

– Geopolitical Supply Chain Constraints: Disruptions in the global supply of specialized alloys or electronics components can impact production schedules.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 1,175,000 KRW

🎯 Target Price: 1,680,000 KRW

Hanwha Aerospace is a premier global defense asset trading at an attractive valuation relative to its high growth profile. The company’s unique capability for rapid delivery, combined with a robust ₩30T+ order backlog, ensures high earnings visibility through the decade. Supported by high-margin export deliveries and dominant aerospace technology, we recommend accumulating shares before full-year 2026 export milestones drive earnings surprises.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*