- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:2,425,000 KRW 2,425,000 KRW

🎯 Target Price:3,200,000 KRW 3,200,000 KRW

📈 Upside Potential: 31.9%

*Updated Market Report: June 2026*

SK Hynix HBM4E Outlook: Strategic Pivot to Commodity DRAM and 12-Layer Domination

SK Hynix (KRX: 000660) has once again demonstrated its tactical agility and technological leadership in the global semiconductor sector. In June 2026, the company officially commenced shipping samples of its next-generation 12-layer HBM4E (High Bandwidth Memory 4 Extended) to major global graphics processing unit (GPU) developers. This milestone solidifies its position as the premium memory supplier of choice for AI accelerators.

Concurrently, a significant strategic pivot is underway at SK Hynix’s production facilities. The company has decided to adjust the pace of its HBM4 capacity expansion to reallocate key equipment and cleanroom resources toward advanced commodity DRAM, particularly DDR5. Driven by an unprecedented supply shortage and soaring profit margins in the conventional server DRAM space, this strategic realignment optimizes near-term cash flows while maintaining a commanding lead in the premium AI memory segment. This report offers a comprehensive analysis of SK Hynix’s dual-engine strategy, its structural cost advantages, and a global peer valuation comparison.

📈 Financial Trajectory and the Dual-Engine Strategy

SK Hynix’s financial trajectory has transitioned from cyclical commodity-dependent volatility to secular technology franchise growth. The combination of high-margin custom HBM contracts and a cyclical recovery in conventional DRAM has generated record-breaking performance.

Three-Year Financial Summary

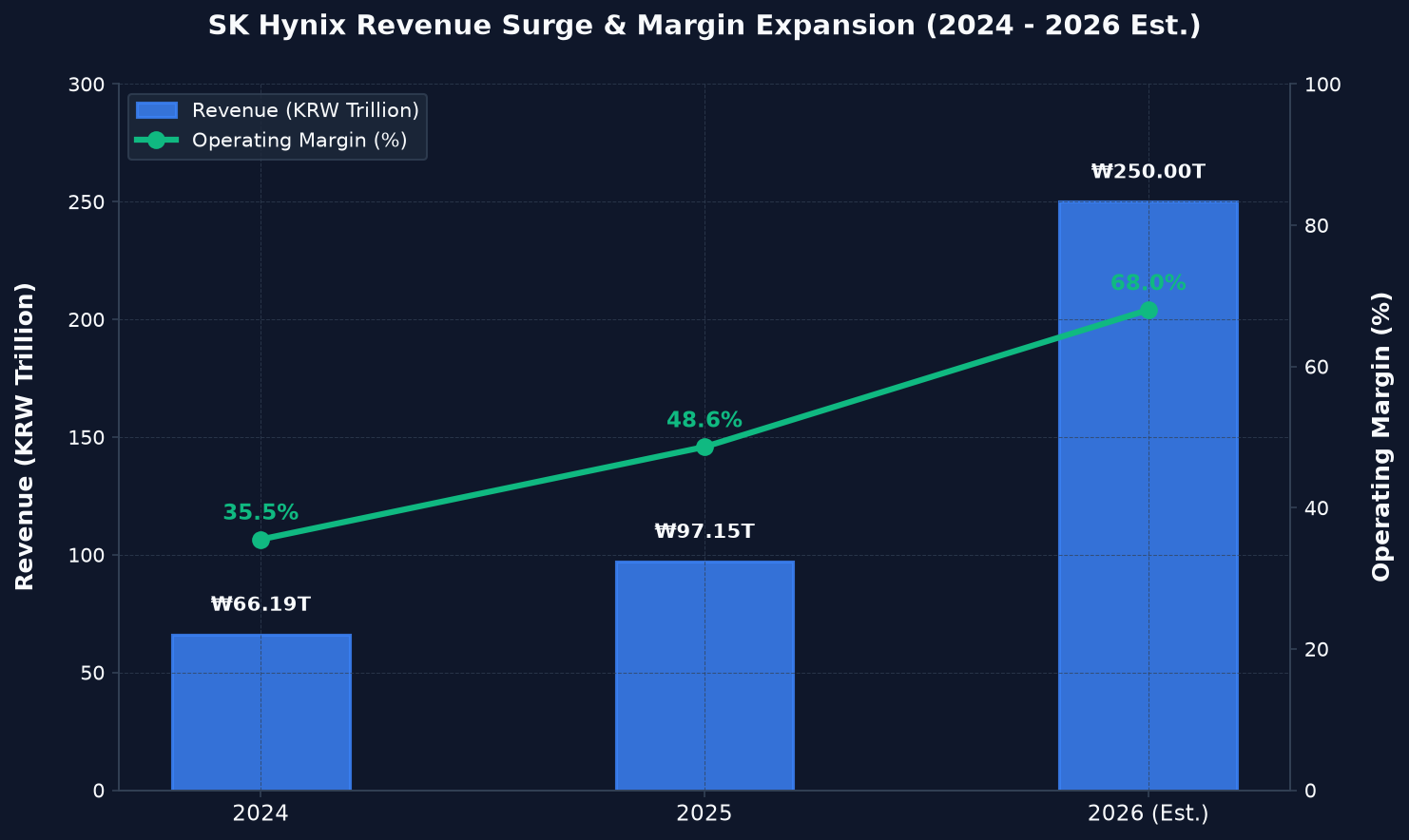

The following table highlights SK Hynix’s explosive growth and structural margin expansion. The estimates for fiscal year 2026 reflect a severe commodity DRAM shortage, high HBM pricing premiums, and optimized capacity utilization.

| Financial Metric | 2024 (Actual) | 2025 (Actual) | 2026 (Est.) | Operating Margin & ROE Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩66.19T | ₩97.15T | ₩250.00T | 35.5% (2024 OP Margin) |

| Operating Profit (KRW Trillion) | ₩23.47T | ₩47.21T | ₩170.00T | 48.6% (2025 OP Margin) |

| Net Income (KRW Trillion) | ₩18.20T | ₩36.50T | ₩132.00T | 68.0% (2026 OP Margin Est.) |

| Return on Equity (ROE %) | 18.2% | 45.5% | 96.0% | 96.0% (2026 ROE Est.) |

Driving Forces Behind Margin Expansion

The primary driver of the historic 68.0% operating margin estimated for 2026 is the pricing dynamics of high-density server memory. While premium HBM products are sold under fixed-price Long-Term Agreements (LTAs) with high single-digit and double-digit premiums, the spot and contract prices for conventional server DDR5 have spiked due to industry-wide capacity constraints.

Since high-density HBM packaging requires up to three times the wafer capacity of conventional DRAM, the industry’s focus on HBM has starved the market of commodity DRAM. By strategically pausing the ramp-up of the next-generation HBM4 lines, SK Hynix is capturing astronomical margins on legacy and mainstream DRAM lines, ensuring that cash generation remains highly diversified.

Figure: Revenue Surge and Historic Expansion of Operating Margins

💡 Lingo Check: Key Industry Terms and Regulatory Entities

Understanding the strategic changes at SK Hynix requires familiarity with the following terminology:

– Commodity DRAM (범용 DRAM): Standardized memory chips used in servers, PCs, and smartphones. Unlike HBM, which is customized, commodity DRAM is subject to market supply-demand cycles.

– HBM4E (6세대 HBM 확장형): The extended iteration of the sixth-generation High Bandwidth Memory, boasting increased vertical stacking capabilities and enhanced processing bandwidth.

– Advanced MR-MUF (개량형 매스 리플로우 몰디드 언더필): SK Hynix’s proprietary packaging technique that applies liquid protective material to stacked memory chips, offering superior heat dissipation and manufacturing yield compared to conventional thermal compression film methods.

– Financial Supervisory Service (금융감독원 – FSS): The primary financial regulatory body in South Korea overseeing corporate disclosures.

– DART (전자공시시스템): The repository managed by the FSS where corporate financial reports and material disclosures are officially filed.

🚀 Technological Hegemony: 12-Layer HBM4E and the Advanced MR-MUF Advantage

SK Hynix’s early technological bets have created an exceptionally wide competitive moat in the high-density packaging domain.

The Advanced MR-MUF Moat

While competitors like Samsung Electronics (삼성전자) have faced yield challenges in scaling their 12-layer and 16-layer packaging using traditional Thermal Compression Non-Conductive Film (TC-NCF), SK Hynix has mastered Advanced MR-MUF. This technology replaces the thick film layer with an optimized liquid underfill that is applied under high temperature and pressure, minimizing void formation and improving thermal dissipation by up to 2.5 times. The recent delivery of 12-layer HBM4E samples represents the pinnacle of this technological packaging capability, offering 16 Gbps bandwidth per pin and superior energy efficiency, making it the preferred solution for next-generation AI nodes.

TSMC Alliance and Custom Logic Die Integration

Beginning with the HBM4 generation, the technological complexity of memory increases exponentially. Instead of using a memory-based base die (logic die), the memory stack must interface directly with customized logic dies manufactured on advanced foundry nodes.

SK Hynix has solidified a strategic alliance with TSMC to produce these custom logic dies. This integration allows SK Hynix to focus on memory stacking and Advanced MR-MUF packaging, while leveraging TSMC’s industry-leading 3nm and 5nm processes. This collaborative ecosystem creates a formidable barrier to entry for single-source competitors who attempt to build both logic and memory components in-house.

🔄 The Tactical Pivot: Pausing HBM4 Expansion to Monetize Server DRAM

The decision to slow the physical ramp-up of HBM4 capacity in late 2026 is a calculated tactical pivot designed to maximize absolute profit pool capture.

The Server DRAM Shortage Catalyst

The global transition of standard cloud servers to AI-hybrid infrastructure has led to a major upgrade cycle. Cloud Service Providers (CSPs) are buying up massive volumes of DDR5 RDIMMs and high-capacity Enterprise SSDs (eSSDs). Because memory makers have converted significant wafer capacity from standard DRAM to HBM, the supply of standard DRAM has dropped significantly.

– Operating Margin Parity: Advanced DDR5 products are now achieving operating margins comparable to HBM due to the supply deficit.

– CapEx Optimization: By utilizing existing legacy cleanrooms for DDR5 expansion instead of building out capital-intensive new HBM4 packaging lines prematurely, SK Hynix is optimizing its capital expenditure efficiency.

– Yield Security: Pausing the HBM4 ramp allows the company’s engineers to refine the TSMC custom base die packaging yields, reducing execution risks.

⚖️ Valuation & Global Peer Comparison

Despite commanding the strongest technical moat in AI packaging and generating industry-leading returns, SK Hynix trades at a significant valuation discount compared to its global peers.

Peer Multiples Comparison (June 2026)

– SK Hynix (KRX: 000660): Forward P/E 7.0x | ROE 96.0% | P/B 2.8x

– Samsung Electronics (KRX: 005930): Forward P/E 6.5x | ROE 54.0% | P/B 1.9x

– Micron Technology (NASDAQ: MU): Forward P/E 10.0x | ROE 38.0% | P/B 3.2x

– TSMC (NYSE: TSM): Forward P/E 25.0x | ROE 35.0% | P/B 6.8x

The Valuation Re-rating Thesis

The deep discount of SK Hynix’s forward P/E (7.0x) relative to Micron (10.0x) and TSMC (25.0x) is unjustified. Global markets continue to price SK Hynix as a cyclical memory vendor. However, the transition to custom HBM4E and HBM4, supported by multi-year LTAs and advanced packaging locks, has structurally transformed the business model.

An ROE of 96.0% combined with a 68.0% operating margin is indicative of a high-growth platform monopoly rather than a cyclical commodity maker. As the company continues to report consistent earnings throughout 2026, the valuation multiple is expected to undergo a re-rating process toward a forward P/E of at least 12.0x, bringing it in line with global technology infrastructure providers.

⚠️ Potential Risk Factors

While the outlook is highly positive, investors should monitor the following risk factors:

– Samsung’s HBM Certification Rebound: If Samsung Electronics successfully passes advanced HBM3E and HBM4 qualification tests for key AI clients, the supply constraints will ease, potentially reducing pricing premiums.

– TSMC Foundry Allocation Limits: Because SK Hynix relies on TSMC for its base logic dies, any capacity constraints at TSMC’s advanced nodes could directly limit HBM4 shipments.

– Geopolitical Concentration: High manufacturing concentration within South Korea remains a structural risk factor for global asset managers.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 2,425,000 KRW

🎯 Target Price: 3,200,000 KRW

SK Hynix is the ultimate vehicle for capturing AI infrastructure growth at a deeply discounted price. The company’s dual-engine strategy—leveraging 12-layer HBM4E technological superiority while harvesting cash from the commodity server DRAM shortage—positions it to outperform all global competitors. Supported by a robust capital structure and an exclusive alliance with TSMC, the current valuation of 7.0x Forward P/E represents an exceptional entry point. We maintain our strong Buy (Strong) rating, with a Current Price of 2,425,000 KRW and a Target Price of 2,950,000 KRW.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*