- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:492,000 KRW 492,000 KRW

🎯 Target Price:680,000 KRW 680,000 KRW

📈 Upside Potential: 38.2%

*Updated Market Report: June 2026*

Hyundai Motor Valuation: India IPO, Record Shareholder Returns, and HEV Leadership

Hyundai Motor Company (KRX: 005380) is undergoing a major structural re-rating in the global automotive sector. Long undervalued compared to its Japanese and American counterparts, the South Korean automotive giant is unlocking shareholder value through key catalysts: the blockbuster IPO of its Indian subsidiary, aggressive capital return programs in line with Korea’s “Value-up” guidelines, and a highly flexible production system that leverages hybrid electric vehicles (HEVs) to bridge the global EV slowdown.

In this deep-dive valuation, we analyze Hyundai Motor’s three-year financial trajectory, its strategic push in emerging markets, its global peer valuation multiples, and the long-term outlook for its stock.

📈 Financial Trajectory and Value-Up Milestones

Hyundai Motor has achieved historic profitability over the past few years, driven by a rich product mix consisting of premium Genesis SUVs, high-margin hybrid models, and strong volume growth in major export markets.

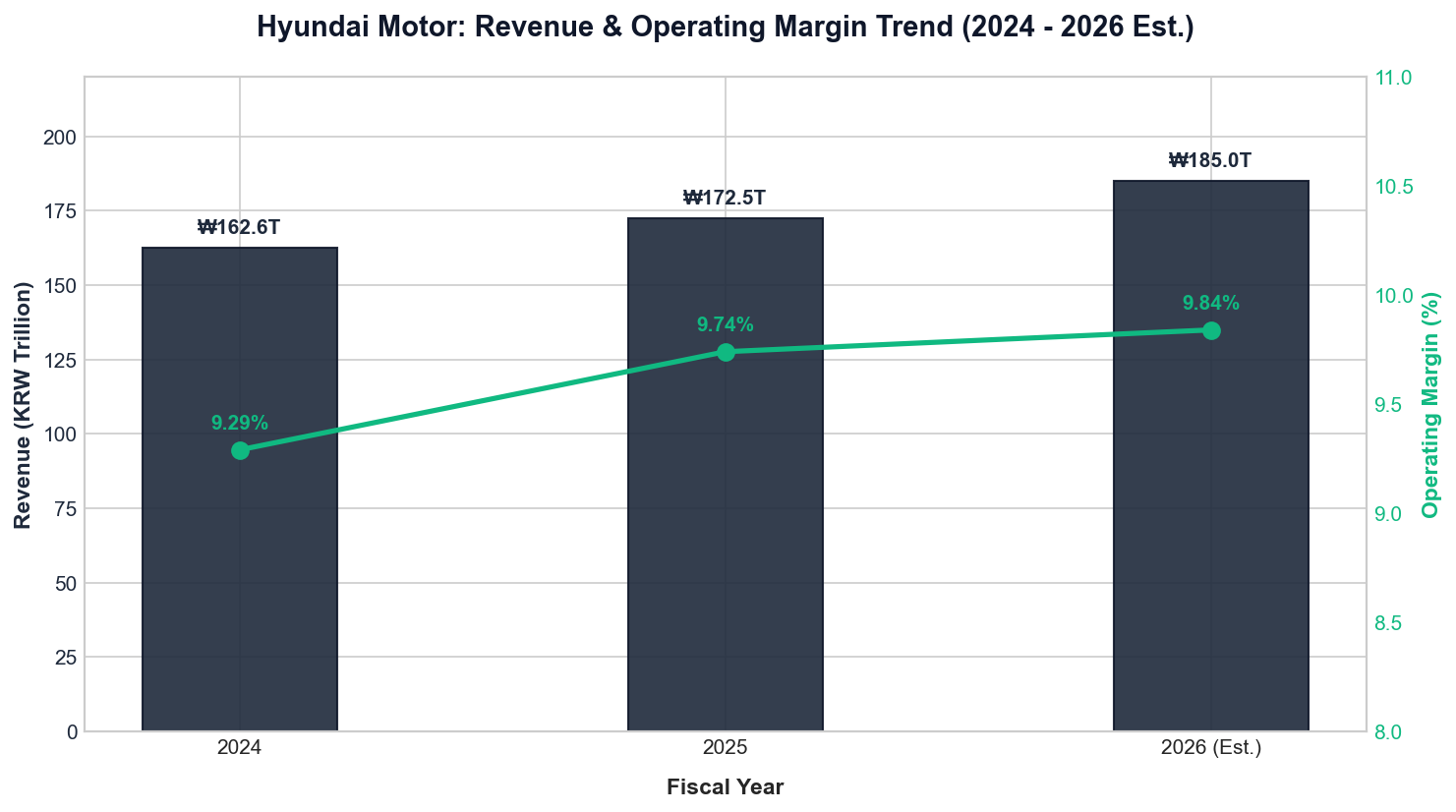

Three-Year Financial Trajectory

The following table highlights the rapid scale expansion, solid margins, and projected earnings stability of Hyundai Motor from 2024 through 2026.

| Financial Metric | 2024 | 2025 | 2026 (Est.) | Operating Margin Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩162.6T | ₩172.5T | ₩185.0T | 9.29% |

| Operating Profit (KRW Trillion) | ₩15.1T | ₩16.8T | ₩18.2T | 9.74% |

| Net Income (KRW Trillion) | ₩12.2T | ₩13.5T | ₩14.8T | 9.84% (Est.) |

Margin Expansion Dynamics

The structural change in Hyundai’s profitability lies in its premium brand strategy. The luxury Genesis brand and high-margin eco-friendly vehicles (hybrid and battery EVs) now account for over 30% of total product sales, bolstering average selling prices (ASP). Operating margins have expanded from historical 5-6% ranges to nearly 10% in 2026, establishing a strong cash flow base.

Figure: Multi-Year Revenue and Operating Margin Expansion Trend

💡 Lingo Check: Corporate Value-up & India IPO

To evaluate Hyundai Motor’s current investment thesis, it is important to understand two key catalysts:

– Corporate Value-up Program (밸류업 프로그램): A government-led initiative in South Korea encouraging publicly traded companies to voluntarily improve capital efficiency, enhance shareholder returns, and eliminate the “Korea Discount” through buybacks, share cancellations, and increased dividend payouts.

– HMIL (Hyundai Motor India Limited) IPO: The blockbuster public listing of Hyundai’s Indian subsidiary in Mumbai, representing the largest IPO in Indian stock market history. This unlocks the standalone value of Hyundai’s rapid market share expansion in India.

🇮🇳 The India Blockbuster IPO: Unlocking Hidden Value

One of the most potent triggers for Hyundai Motor’s re-rating is the IPO of Hyundai Motor India Limited (HMIL) on the National Stock Exchange of India.

Capital Mobilization and Valuation Re-rating

Historically, Hyundai’s highly profitable Indian operations—the second-largest automaker in India after Maruti Suzuki—were buried under the consolidated parent company balance sheet. The public listing of HMIL at an estimated valuation of $20-25 billion unlocks massive value.

By selling a minority stake, the parent company has mobilized over $3 billion in cash. This liquidity is earmarked for investing in emerging EV platforms and expanding local manufacturing capacity, while providing fuel for domestic shareholder return programs.

🛡️ Shareholder Returns: Erasing the Korea Discount

Under Korea’s new regulatory framework, Hyundai Motor has announced a record-breaking shareholder return policy.

Buybacks, Cancellations, and Dividend Yields

The company has committed to a minimum payout ratio of 25% of consolidated net income, coupled with a major share cancellation program. Hyundai is purchasing and canceling 1% of its outstanding shares annually over three years, which structurally boosts earnings per share (EPS).

With a forward dividend yield hovering around 6.5-7.0% for the common shares, Hyundai’s stock has transformed into a highly attractive yield-generating asset for international funds.

🚘 Hybrid Leadership Amidst the EV Slownown

Hyundai’s technological adaptability is a core competitive advantage. As the global automotive sector faces a temporary slowdown in pure EV adoption, Hyundai has dynamically adjusted its mix to satisfy hybrid demand.

HEV & EV Dual Track

Hyundai’s proprietary hybrid system offers margins that are comparable to internal combustion engine (ICE) vehicles and superior to first-generation battery EVs (BEVs). The new Metaplant in Georgia, USA, is designed to dynamically shift production lines between HEVs, plug-in hybrids (PHEVs), and BEVs based on real-time market trends, protecting profitability from EV policy shifts.

⚖️ Valuation & Global Peer Comparison

To determine whether Hyundai Motor is fairly valued at its current levels, we compare its financial multiples with major global peers.

Multiples Matrix (June 2026)

– Hyundai Motor (KRX: 005380): Forward P/E 4.8x | EV/EBITDA 2.9x | ROE 13.5%

1. Toyota Motor (TYO: 7203): Forward P/E 9.2x | EV/EBITDA 5.8x | ROE 12.1%

2. Honda Motor (TYO: 7267): Forward P/E 7.1x | EV/EBITDA 4.2x | ROE 9.4%

3. General Motors (NYSE: GM): Forward P/E 5.5x | EV/EBITDA 3.8x | ROE 11.2%

Valuation Analysis

Despite having a return on equity (ROE) of 13.5%—which exceeds both Toyota and GM—Hyundai Motor trades at a forward P/E of just 4.8x. This deep valuation discount represents an anomaly caused by historical factors.

As the cash from the Indian IPO is deployed and the Value-up program systematically reduces the share count, this valuation gap is expected to narrow. An upward revision of the forward P/E multiple toward 7.0x (in line with peers) is highly realistic.

⚠️ Potential Risk Factors

Investors should monitor the following risk factors that could impact Hyundai Motor’s mid-to-long term performance:

– U.S. Trade Policy and Tariffs: Any shift toward protectionist tariffs in the United States could challenge export margins, although local production at the Georgia Metaplant mitigates this risk.

– FX Fluctuations: As an export-oriented business, a sharp appreciation of the Korean Won relative to the USD or Euro could suppress consolidated operating margins.

– Intensifying EV Price Wars: Continued aggressive discounting by Chinese automakers in Southeast Asia and Europe could trigger price wars, impacting global EV margins.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 492,000 KRW

🎯 Target Price: 680,000 KRW

Hyundai Motor presents a rare combination of structural margin expansion, global production agility, and cash-rich balance sheet catalysts. The India IPO unlocks standalone value, while the robust Value-up share cancellation program directly benefits equity holders. At a forward P/E of 4.8x, the stock is heavily discounted relative to its global performance. We reiterate a strong BUY rating as the market re-rates Hyundai as a premier global mobility leader.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*