- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:362,500 KRW 685,000 KRW

🎯 Target Price:520,000 KRW 920,000 KRW

📈 Upside Potential: 43.4%

*Updated Market Report: June 2026*

LG Energy Solution Valuation: Bridging the EV Chasm with ESS and Next-Gen Battery Dominance

LG Energy Solution (KRX: 373220), South Korea’s leading pure-play lithium-ion battery manufacturer, is navigating a pivotal transition in the global clean energy supply chain. As the automotive industry experiences a temporary cooling in pure electric vehicle (EV) sales—a phenomenon widely described as the “EV Chasm”—LG Energy Solution has pivotally shifted resources toward stationary Energy Storage Systems (ESS) for public utilities and the mass production of next-generation 46-series cylindrical cells.

This strategic adaptability, coupled with massive tax credits under the U.S. Inflation Reduction Act (IRA), is helping the company maintain premium valuations compared to its Chinese and Japanese counterparts. This report delivers a detailed valuation analysis of LG Energy Solution, evaluating its three-year financial trajectory, ESS growth contribution, next-gen cell roadmaps, and relative multiples against global peers.

📈 Financial Trajectory and the ESS Pivot

LG Energy Solution’s income statement reflects the impact of the global EV transition. While top-line growth slowed during the 2024-2025 period due to high interest rates and battery metal price corrections, the company’s operating profitability has rebounded significantly.

Three-Year Financial Summary

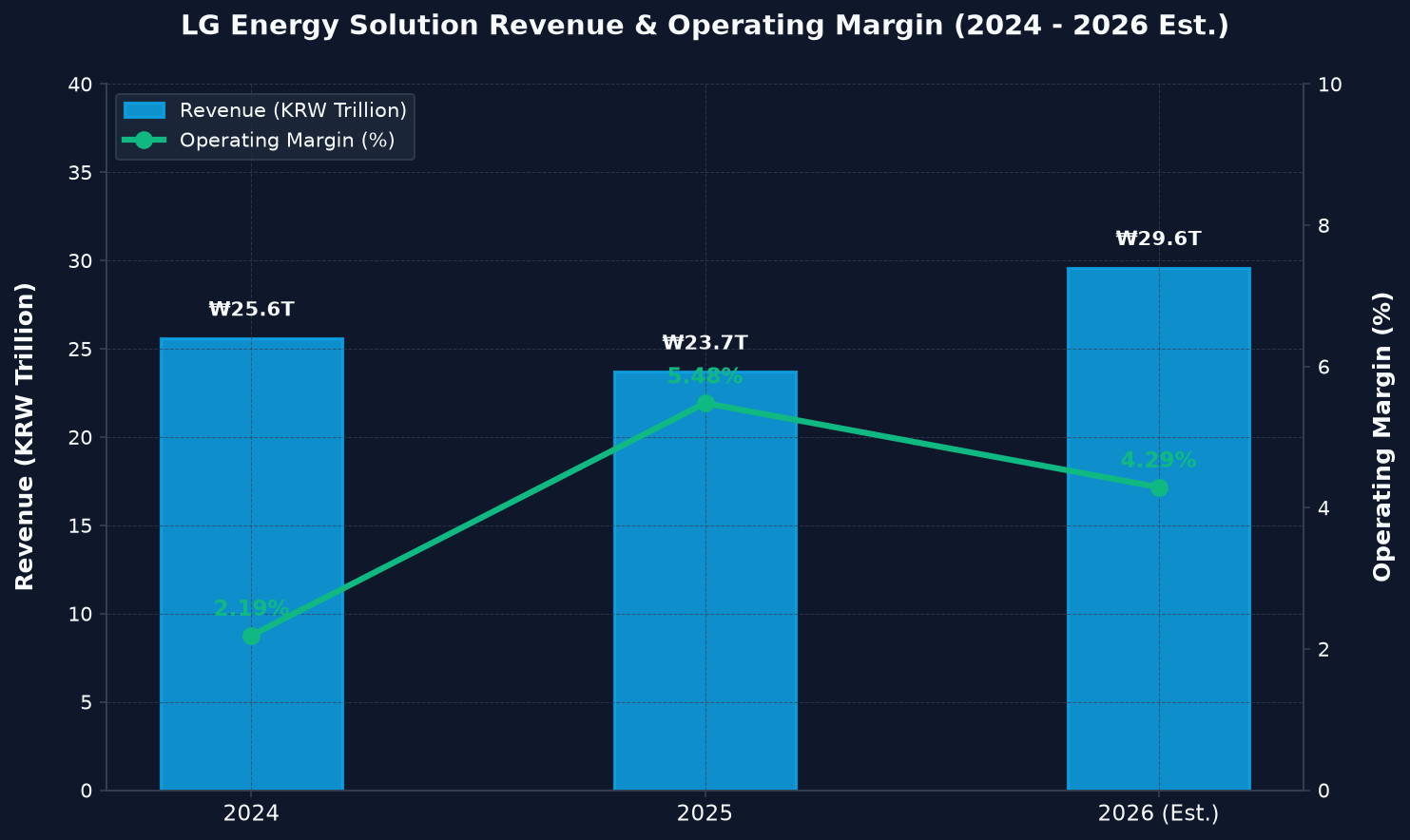

The following table outlines LG Energy Solution’s financial performance from 2024 through 2026 estimates. The figures for 2026 reflect the strategic shift toward high-margin utility-scale ESS shipments and initial sales of 4680 cylindrical cells.

| Financial Metric | 2024 (Actual) | 2025 (Actual) | 2026 (Est.) | Operating Margin & ROE Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩25.60T | ₩23.70T | ₩29.60T | 2.19% (2024 OP Margin) |

| Operating Profit (KRW Trillion) | ₩0.56T | ₩1.30T | ₩1.27T | 5.48% (2025 OP Margin) |

| Net Income (KRW Trillion) | ₩0.40T | ₩0.92T | ₩0.90T | 4.29% (2026 OP Margin Est.) |

| Return on Equity (ROE %) | 1.80% | 3.90% | 5.50% | 5.50% (2026 ROE Est.) |

Profitability Drivers and CapEx Maturation

The main driver behind the recovery of operating profit in 2025 and 2026 is the expansion of utility-scale energy storage products in North America. These products utilize LFP (Lithium Iron Phosphate) chemistries manufactured locally, qualifying them for robust federal incentives. Additionally, the company’s capital expenditure (CapEx) cycle is beginning to mature.

Having completed the initial construction of massive joint-venture plants with General Motors, Honda, and Stellantis, the company is shifting from heavy investment to optimizing capacity utilization, structurally reducing depreciation drag on margins.

Figure: Revenue Recovery and Operating Margin Trend (2024 – 2026 Est.)

💡 Lingo Check: Battery Policy and Disclosure Bodies

To understand LG Energy Solution’s operational framework, it is helpful to outline key regulatory terms:

– IRA AMPC (첨단 제조 생산 세액공제): Advanced Manufacturing Production Credit under the U.S. Inflation Reduction Act, which awards battery manufacturers $35 per kilowatt-hour (kWh) for battery cells and $10 per kWh for modules produced in the United States.

– ESS (에너지 저장 시스템): Energy Storage Systems designed to store electrical power on a utility scale, commonly integrated with renewable energy sources like wind and solar to stabilize grid systems.

– Financial Supervisory Service (금융감독원 – FSS): The primary government body in South Korea overseeing corporate transparency and market disclosures.

– DART (전자공시시스템): The electronic disclosure system operated by the FSS, where Korean corporations file official financial statements.

🔋 Technology Roadmap: 46-Series Cylindrical Batteries and LFP Pivot

LG Energy Solution is deploying two key technological strategies to navigate the changing battery market.

Cylindrical 46-Series Dominance

LG Energy Solution has established an early lead in mass-producing the 46-series cylindrical cells (specifically 4680 cells), which are becoming the standard format for major EV manufacturers including Tesla. By starting production at its dedicated Ochang plant in South Korea in late 2024 and expanding to North American sites in 2026, LGES is securing long-term high-margin supply agreements. These cylindrical cells offer five times the energy capacity and six times the power of standard 2170 cells, providing a substantial advantage over competitors who are still struggling with early-stage yield rates.

The LFP Battery Transition for ESS

To compete with low-cost Chinese cell makers in the stationary energy storage market, LG Energy Solution has developed its own Lithium Iron Phosphate (LFP) pouch cells. By producing these cells at its Arizona plant in the United States, the company avoids tariffs applied to Chinese battery imports while capturing the IRA AMPC benefits. This allows LGES to offer competitive pricing to North American utility clients while maintaining positive margin spreads.

🔄 EV Chasm Mitigation Strategy: Deploying Grid Infrastructure

The core of LG Energy Solution’s near-term recovery is its strategic focus on stationary utility-scale energy storage.

The AI Data Center Demand Trigger

The rapid global build-out of artificial intelligence data centers has created an unprecedented demand for continuous electricity. Since grids cannot rely solely on intermittent solar and wind power, utility-scale battery systems are essential to prevent grid instability.

– Portfolio Shift: LG Energy Solution has stated its goal to increase the revenue share of its ESS business to mid-30% by the end of 2026, up from low single digits in 2023.

– High Backlog Visibility: Over 70% of the company’s Arizona plant capacity for ESS is pre-sold through long-term supply agreements with major U.S. power developers, providing highly predictable cash flows.

– High-margin Upgrades: The company integrates advanced liquid cooling systems and energy management software into its containerized ESS products, capturing software-like premium margins.

⚖️ Valuation & Global Peer Comparison

Despite navigating the EV transition and possessing a strong manufacturing presence in the United States, LG Energy Solution trades at a significant premium compared to global peers.

Valuation Multiples Matrix (June 2026)

– LG Energy Solution (KRX: 373220): Forward P/E 87.6x | EV/EBITDA 28.2x | ROE 5.5%

– CATL (SZSE: 300750): Forward P/E 31.9x | EV/EBITDA 16.5x | ROE 22.0%

– BYD Co. (SZSE: 002594): Forward P/E 27.5x | EV/EBITDA 27.1x | ROE 20.0%

– Panasonic (TSE: 6752): Forward P/E 15.5x | EV/EBITDA 14.3x | ROE 7.0%

Valuation Analysis and the Multiples Premium

LG Energy Solution’s high Forward P/E of 87.6x and EV/EBITDA of 28.2x compared to CATL (31.9x P/E) is a reflection of its unique geopolitical position. Unlike Chinese battery makers who face steep tariffs (up to 25% under U.S. Section 301 tariffs), LGES enjoys tariff-free access to the North American market.

Additionally, the company’s operating profit is highly dependent on the IRA AMPC. For example, in its recent financial disclosures on DART, the company’s operating profit would have been negative without the AMPC subsidies. As global EV demand recovers and the high-margin ESS business scales, the company’s earnings per share (EPS) are projected to grow rapidly, which will naturally compress the P/E multiple toward historical averages. Until then, the premium valuation is justified by its protected position in the U.S. supply chain.

⚠️ Potential Risk Factors

Investors should monitor the following risk factors that could impact LG Energy Solution’s performance:

– IRA Policy Volatility: Any legislative attempts to scale back or repeal the IRA AMPC subsidies in the United States would significantly impact the company’s operating profits.

– LFP Cost Competition: Continued price cuts on LFP chemistries by Chinese competitors could force LGES to lower its prices, impacting margins despite domestic subsidies.

– Execution Risks in Advanced Cylindrical Cells: Any yield or ramp-up delays in 4680 cell production at North American sites could slow shipment volumes and impact contract relationships.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 362,500 KRW

🎯 Target Price: 520,000 KRW

LG Energy Solution represents a premium investment option in the global battery sector, protected by its strategic positioning in the U.S. market. While the EV Chasm continues to impact near-term volume growth, the rapid expansion of the utility-scale ESS business and the scaling of next-generation 4680 cells provide strong recovery catalysts. Although the current Forward P/E of 87.6x appears elevated, it reflects a temporary dip in earnings that is set to recover as factory utilization rates normalize. We recommend accumulating shares on market weakness, with a target price of ₩480,000.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*