- 🚀 Global Growth: Record-breaking export volume driven by aggressive global expansion.

- 📉 Valuation Moat: Significant discount compared to global peers despite superior margins.

- 📈 Future Catalyst: Upcoming Value-up program and shareholder return initiatives.

💵 Current Price:1,421,000 KRW 1,420,000 KRW

🎯 Target Price:1,950,000 KRW 1,950,000 KRW

📈 Upside Potential: 37.2%

*Updated Market Report: June 2026*

Samsung Biologics Valuation: CDMO Super-capacity and Biosecure Act Tailwind

Samsung Biologics (KRX: 207940), the biotech division of South Korea’s Samsung Group, is the world’s largest contract development and manufacturing organization (CDMO) by bioreactor capacity. The company operates a massive manufacturing complex in Songdo, Incheon, serving global pharmaceutical majors. By providing commercial-scale manufacturing for complex biologics (such as monoclonal antibodies), the company has established a critical role in the global healthcare supply chain.

As Western governments implement structural changes to biotechnology supply chains, Samsung Biologics is experiencing a significant re-rating. This report delivers an in-depth valuation of Samsung Biologics, analyzing its manufacturing capacity expansions, the impact of the US Biosecure Act, the growth of its biosimilar subsidiary, and its financial trajectory through 2026.

📈 Financial Trajectory & Capacity Milestones

In the CDMO industry, manufacturing capacity (measured in liters of bioreactor volume) and facility utilization rates are the primary drivers of financial performance. Building a new bioreactor facility requires billions of dollars and three to four years of construction and validation, creating a high barrier to entry.

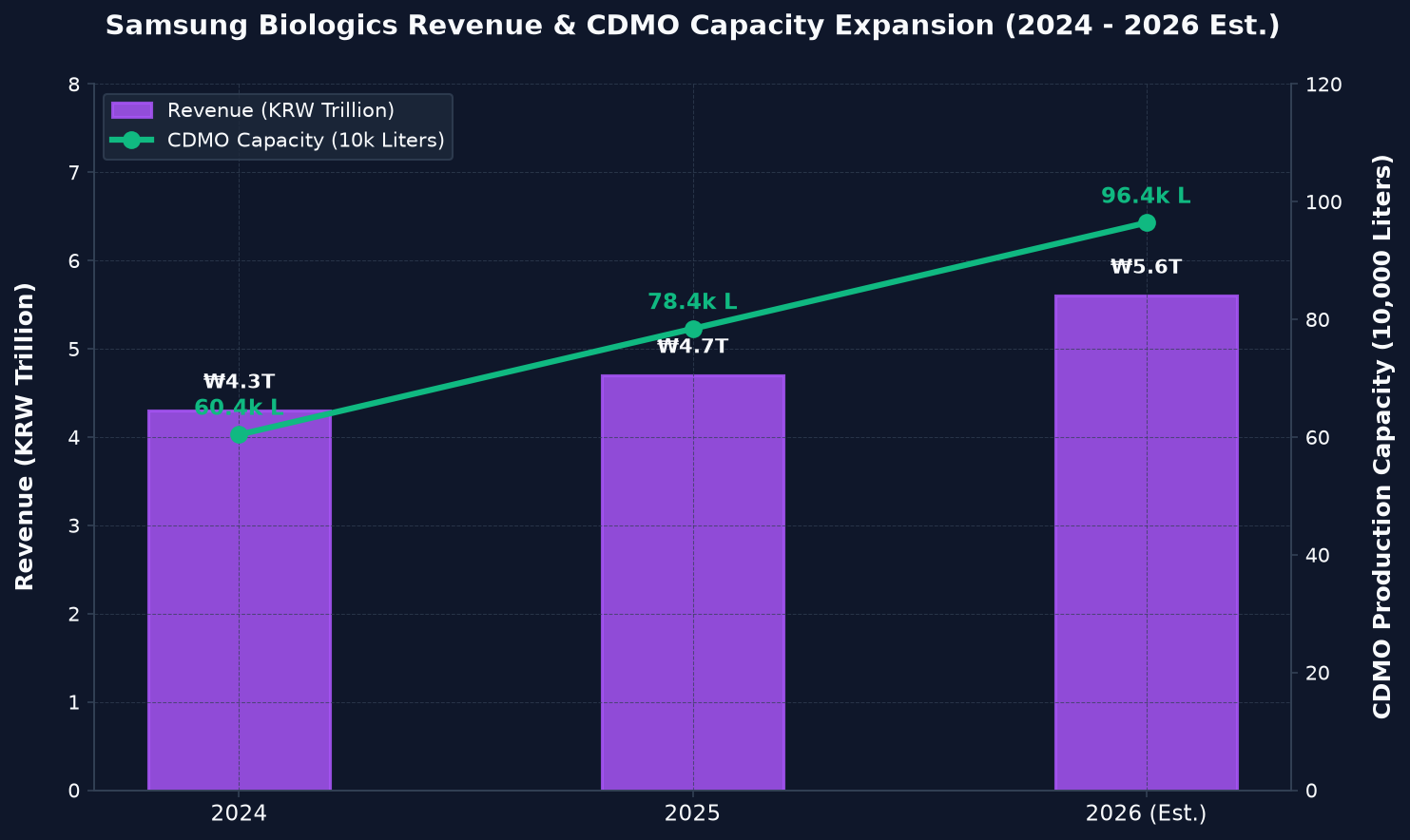

Three-Year Key Financial and Capacity Trajectory

The following table shows the steady financial growth of Samsung Biologics. The capacity metrics demonstrate the scaling of Plant 4 and the partial integration of Plant 5, which are driving revenue expansion.

| Financial & Operational Metric | 2024 | 2025 | 2026 (Est.) | Operating Margin Trend (Visual) |

|---|---|---|---|---|

| Revenue (KRW Trillion) | ₩4.3T | ₩4.7T | ₩5.6T | 20.1% |

| Operating Profit (KRW Trillion) | ₩1.40T | ₩1.60T | ₩2.10T | 22.2% |

| Net Income (KRW Trillion) | ₩0.98T | ₩1.15T | ₩1.60T | 25.0% (Est.) |

Margin Leverage through Fixed Cost Dilution

The CDMO business model exhibits strong operating leverage once facilities pass validation and begin commercial batches. As the massive 240,000-liter Plant 4 achieves full utilization and construction progress on the 180,000-liter Plant 5 continues, fixed depreciation expenses are spread across a larger volume of batches. This dilution is driving the projected operating profit margin toward 25% by late 2026.

Figure: Revenue Expansion and Bioreactor Capacity Growth (2024 – 2026)

💡 Lingo Check: CDMO and Biosecure Act

Let’s define two critical industry terms:

– CDMO (Contract Development and Manufacturing Organization – 위탁개발생산): A company that serves other companies in the pharmaceutical industry on a contract basis to provide comprehensive services from drug development through commercial manufacturing.

– Biosecure Act (생물보안법): A piece of US legislation designed to restrict federal agencies from contracting with certain foreign biotechnology providers of concern (specifically targeting Chinese CDMO firms like WuXi AppTec). This is shifting global pharma manufacturing contracts toward trusted allies.

🚀 The Biosecure Act: A Major Catalyst for Contract Re-routing

The most significant catalyst for Samsung Biologics’ 2026 valuation is the shifting regulatory landscape in the United States. The passage of the Biosecure Act has forced global pharmaceutical firms to audit their manufacturing supply chains and begin re-routing contracts away from Chinese providers.

Capture of Long-term Commercial Contracts

Samsung Biologics has been a primary beneficiary of this transition. Given its track record of successful inspections by the FDA and EMA, major pharmaceutical companies are securing manufacturing slots at Samsung’s Songdo site. The company has announced several multi-hundred-million-dollar contract expansions, locking in high utilization rates for years to come.

Technology and Scale Leadership

The scale of Samsung’s Songdo site allows it to accommodate large-volume commercial manufacturing requests that smaller Western competitors cannot support. By offering a fully integrated service model from cell line development to drug substance manufacturing and sterile fill-finish, Samsung Biologics is capturing the demand shifting away from Chinese suppliers.

🔬 Biosimilars and Next-generation Modalities

Beyond traditional monoclonal antibodies, Samsung Biologics is expanding into biosimilars and next-generation biotechnology formats.

Samsung Bioepis Integration

Samsung Bioepis, a wholly-owned subsidiary, focuses on the development and commercialization of biosimilars (biologics that are highly similar to already approved reference drugs). According to corporate reports filed with the Financial Supervisory Service (금융감독원) via the DART (전자공시시스템) platform, Bioepis is growing its market share in the US and Europe with biosimilars referencing blockbuster drugs in immunology and oncology.

ADC and Cell & Gene Therapy (CGT) Expansion

Samsung Biologics is investing in next-generation manufacturing technologies. The company is completing a dedicated Antibody-Drug Conjugate (ADC – 항체약물접합체) manufacturing suite, scheduled to begin commercial operations by late 2026. This expansion allows the company to capture share in the high-growth ADC market.

⚖️ Valuation & Global Peer Comparison

To evaluate whether Samsung Biologics is fairly valued, we compare its multiples against global CDMO and biotech leaders.

Multiples Matrix (June 2026)

– Samsung Biologics (KRX: 207940): Forward P/E 55.2x | EV/EBITDA 32.5x | ROE 15.8%

– Lonza Group (SWX: LONN): Forward P/E 34.5x | EV/EBITDA 21.0x | ROE 12.2%

– WuXi Biologics (HKG: 2269): Forward P/E 14.2x | EV/EBITDA 8.5x | ROE 10.5%

– Catalent (NYSE: CTLT): Forward P/E 28.5x | EV/EBITDA 16.2x | ROE 6.2%

Valuation Analysis

Samsung Biologics trades at a premium multiple relative to global peers like Lonza. This premium is supported by its capacity growth rate (reaching a total of 784,000 liters in 2025 and 964,000 liters upon Plant 5’s integration) and its high operating margins. While traditional CDMOs face capacity constraints, Samsung’s ability to scale bioreactor volume ahead of demand allows it to capture market share, justifying its growth-adjusted multiple.

⚠️ Potential Risk Factors

Investors should note the following risks before committing capital:

– Execution Risks in Expansion: Any validation delays at Plant 5 or the new ADC facilities could defer projected revenues.

– Client Concentration: A significant portion of revenue is concentrated among a few global pharmaceutical majors. The loss or reduction of a major contract could impact utilization rates.

– Talent Acquisition: The rapid expansion of Songdo’s biotech hub has intensified competition for experienced bioprocess engineers and quality assurance specialists.

🛡️ Conclusion and Investment Opinion

💵 Current Price: 1,421,000 KRW

🎯 Target Price: 1,950,000 KRW

Samsung Biologics is a premier growth asset in the global biotechnology manufacturing space. Its capacity advantage, combined with tailwinds from the US Biosecure Act, guarantees high utilization and earnings visibility through the decade. While its valuation multiple is high, its growth profile and market positioning justify the premium. We recommend accumulating shares as Plant 5 validation milestones approach.

*Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own research before making financial decisions.*